About Galileo Secured Credit

A secured credit card is designed to help cardholders with no credit, thin credit, or poor credit build their credit history—all while minimizing risk to lenders. Common use cases for secured credit cards include young adults or immigrants looking to establish or build their credit history, or those with a poor credit history looking to improve their score.

Here is a brief overview of how secured credit works:

- Application and approval — The customer applies for a secured credit card and is approved.

- Deposit — During enrollment, the cardholder deposits funds to the issuing bank, which backs the credit limit extended to them.

- Card issuance — The cardholder receives a secured credit card.

- Purchase — The cardholder makes purchases with the secured credit card.

- Billing cycle — At the end of the billing cycle, the cardholder is billed for the full amount owed against the credit limit.

- Payment — The cardholder pays the full amount of the credit card bill on time and continues to do so over several months.

- Credit reporting — The payment history is reported to credit bureaus, impacting the cardholder’s credit score.

Galileo’s secured credit product is a charge card product, rather than a conventional revolving credit product. Charge cards have a few key differences:

- The balance is due in full at the end of each billing cycle. Cardholders are not offered a minimum payment, and they cannot carry a balance into the next month.

- If the cardholder does not pay the full amount, lenders can decide to pull funds from the secured account to pay the bill, reducing the issuer's risk of loss.

- Secured credit products do not assess interest.

- Option to assess fees, such as program and late fees.

- The issuer's revenue sources come from interchange and fees (annual, late payments, etc.).

Note that the charge card associated with secured credit is often referred to as a credit card in marketing materials.

Secured Credit models

Galileo offers three secured-credit models to help you design a program that fits your business and customer base:

- Two-Account — This model consists of a Galileo-managed secured deposit account and a credit account. It is best suited for programs that do not offer a debit card program.

- Three-Account — This model consists of a Galileo-managed deposit account, a secured collateral account, and a credit account. The deposit account can be a Galileo DDA or a DDA with another institution.

- Dynamic Funding — This is the most automated secured credit program, which employs a Galileo-managed DDA, a secured collateral account, and a credit account. Dynamic Funding simplifies balance management for cardholders with both a debit card and a secured credit card.

Consult the table of the different features and capabilities for each secured credit model.

| Two-Account | Three-Account | Dynamic Funding | |

|---|---|---|---|

| Galileo-hosted deposit account | Optional | X | |

| Galileo-hosted secured account | X | X | X |

| Galileo-hosted credit account | X | X | X |

| Autopay | Optional | Optional | Optional |

| Automated credit limits | Optional | Optional | X |

| Automated secured account funding | X | ||

| Single funding account for credit and debit | X | ||

| Semi-secured credit | Optional | Optional | |

| Metro 2 file creation | Optional | Optional | Optional |

| Reg Z disputes | X | X | X |

| Authorized users | X | X | |

| Delinquency management | Optional | Optional | Optional |

| Credit statements | Optional | Optional | Optional |

See Setup for Galileo Secured Credit for descriptions of the features and capabilities.

The following sections provide details on the different models.

Two-Account Secured Credit

Two-Account Secured Credit is the simplest secured credit option and is best suited for programs that do not offer a debit card program. In this model, the customer has two Galileo-hosted accounts:

- Deposit account — Holds the collateral funds deposited by the cardholder.

- Credit account — Linked to the credit card, the credit limit is determined by the collateral balance.

How it works

- Collateral deposit — The cardholder deposits funds into the secured deposit account*. This account can receive direct deposit.

- Set the credit limit —The amount in the secured deposit account sets the credit limit for the credit card. For example, if a cardholder deposits 200.00, the credit limit is 200.00. If they deposit an additional 200.00, the credit limit increases to 400.00.

- Purchase — The cardholder makes purchases using the secured credit card. The matching amount of funds is held in the secured deposit account as collateral and cannot be withdrawn except to repay the credit account balance.

- Billing cycle — At the end of the billing cycle, the cardholder is billed for the full amount owed.

- Payment — The cardholder can pay off their credit balance directly from the secured deposit account (reducing their credit limit) or from an external deposit account. Autopay can be enabled to manage payments from a secured collateral account.

Secured deposit accounts cannot be accessed via a debit card due to network regulations.

Cardholder benefits

- Ease of use – With only two accounts and one card, two-account secured credit creates an easier program for cardholders to understand.

- Fund via ACH or direct deposit — Secured deposit accounts accept ACH credits and direct deposits. Direct deposit eliminates the need to manually fund the secured deposit account.

- Access to cash —

- Cardholders can get cash advances from ATMs using the credit card.

- Cardholders can withdraw excess funds from the secured deposit account at any time, as long as the withdrawal amount is less than the difference between the secured deposit account balance and the credit balance.

Program benefits

- Simple market entry — Easy entry into the secured credit market for programs that do not offer a debit program.

- Cost-effectiveness — Most cost-effective for program managers, as it eliminates the need for two cards.

- Credit interchange revenue — Guaranteed credit interchange with every swipe.

Example scenario

The following steps represent Two-Account Secured Credit:

- George is a recent immigrant to the United States. He is unable to obtain a traditional revolving credit card because he does not have a credit history with a U.S. bank. He is interested in a secured credit program with you to help establish and build his credit history.

- George applies and is approved for your secured credit program.

- He decides to set up direct deposit for his secured deposit account, ensuring he can get the highest credit limit possible and maximize his credit spending.

- He is issued a new charge card for the new credit account.

- George makes a purchase of 100.00 using his charge card.

- George pays his bills according to the collateral in his secured deposit account.

- At the end of the month, George’s outstanding balance is due in full. He pays off his balance on time.

- A positive record of his repayment history is sent to the credit bureaus, helping build George’s credit score.

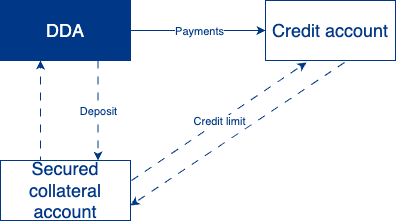

Three-Account Secured Credit

Three-Account Secured Credit is designed to integrate with an existing debit program at your institution. In this model, the customer has three accounts:

- Deposit account — Holds the cardholder’s funds and is accessible via a debit card. This can be a DDA with Galileo or another institution.

- Secured collateral account — Holds the collateral funds deposited by the cardholder.

- Credit account — Linked to the credit card, the credit limit is determined by the collateral balance.

How it works

- Collateral deposit — The cardholder moves funds into the secured collateral account from their deposit account.

- Credit limit — The amount in the secured collateral account sets the credit limit for the credit card. For example, if a cardholder deposits 200.00, the credit limit is 200.00. If they deposit an additional 200.00, the credit limit increases to 400.00.

- Purchase — The cardholder makes purchases using the secured credit card. The matching amount of funds are held in the secured collateral account, unable to be withdrawn except to repay the credit account balance.

- Billing cycle — At the end of the billing cycle, the cardholder is billed for the full amount owed.

- Payment — The cardholder can pay off their credit balance directly from the secured collateral account (reducing their credit limit) or from their external deposit account.

Cardholder benefits

- Flexibility — Inclusion of a debit card provides the cardholder with flexibility with their funds.

- Bi-directional funds transfer — Allows the cardholder to add funds to the secured collateral account to increase the credit limit or remove funds to increase cash reserves.

- Payment management — Allows cardholders to make payments from the secured collateral account.

Program benefits

- Payment management — Programmatically manage payments from the cardholders’ secured collateral account on their behalf without damage to their credit.

- Risk mitigation — You can decide to pull funds from the collateral account and/or close the account in default if a cardholder fails to pay the balance in full.

Example scenario

The following steps represent Three-Account Secured Credit:

- Sally has a checking account with your institution. She is interested in a secured credit program to start building her credit history.

- Sally applies to your secured credit program.

- After you review and approve her application, Sally transfers 500.00 from her checking account into the collateral account that serves as the credit limit on her charge card.

- She activates the card and purchases textbooks for 100.00 using her charge card.

- At the end of her billing cycle, she is billed for the full amount, due on a specified date.

- Sally pays the full amount on time, and a positive record of the billing cycle is sent to the credit bureaus.

- At the end of the next billing cycle, Sally unfortunately misses a payment. In this case, a negative record of the billing cycle is sent to the credit bureaus.

- Sally does not repay her balance and you claim the collateral funds to mitigate/eliminate the loss.

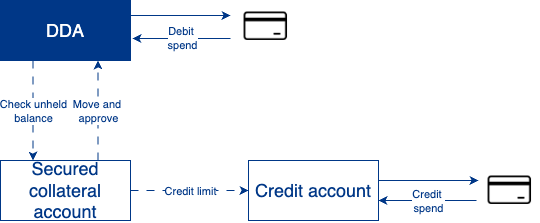

Dynamic Funding

Dynamic Funding mitigates the complexities cardholders have with traditional three-account secured credit models. Typically, cardholders have three account balances to manage, accessed via two different credentials. With Dynamic Funding, Galileo automates funds movement between accounts, creating a model where a cardholder can view a single “available to spend” balance that can be accessed through either their credit or debit card. Due to the automated nature of Dynamic Funding, Galileo must host all three accounts:

- Deposit account — The deposit account balance will routinely be 0.00, as all deposited funds are immediately routed to the collateral account.

- Secured collateral account — Holds the collateral funds deposited by the cardholder.

- Credit account — Linked to the credit card, the credit limit is determined by the collateral balance.

How it works

- Deposit — When a cardholder signs up for dynamic funding, all funds in their deposit account, and all future deposits, will be automatically transferred to the collateral account.

- Credit limit —The amount in the collateral account sets the credit limit for the credit card. Cardholders have the highest credit limit possible since all of their cash is routed to the secured collateral account.

- Credit purchases — The cardholder makes purchases using the secured credit card. The matching amount of funds is held in the secured collateral account and cannot be withdrawn except to repay the credit account balance.

- Debit purchases — The cardholder can pay with cash using the debit card. Although the deposit account has a balance of 0.00, authorizations are checked against the amount in the secured collateral account that is not being used as collateral for credit transactions. These funds are moved to the deposit account in real time to fund the transaction.

- Billing cycle — At the end of the billing cycle, the cardholder is billed for the full amount owed against the credit limit.

- Payment — The cardholder can pay off their credit balance directly from the secured collateral account (reducing their credit limit) or from an external deposit account.

Cardholder benefits

- Immediate approval — Customers can be approved for a secured credit card immediately since they already have funds in a Galileo DDA that can be moved to the collateral account.

- Manage a single balance — Cardholders can access a single balance with their credit or - debit credentials.

- Automated funding — Cardholders do not have to manage their funding as they do in the two and three-account models.

Program benefits

- Bundled credit and debit product offering — Offer your customers a credit and debit combination product.

- Minimal account management — Reduces the need for manual account transfers and adjustments.

- Mitigates risk – Provides first rights to the collateral account funds in the event of default.

- Novel product offering — Offer your customers an innovative secured credit product.

Example scenario

The following steps represent Dynamic Funding:

- Tom applies for a secured credit card program and is approved because he has a DDA account with your institution.

- Tom's 2500.00 paycheck is directly deposited into his Galileo DDA, and the amount is automatically routed to the secured collateral account. The funds are held in the collateral account, fully secured.

- Tom’s deposit account is now 0.00 and the secured credit account balance is 2500.00.

Because the secured credit account balance is 2500.00, Tom’s credit limit is 2500.00. - Tom uses his secured credit card to purchase a new keyboard for 100.00.

Galileo approves the transaction because there are sufficient funds available in the secured collateral account. - The credit spend puts a hold of 100.00 in the collateral account and adjusts the available credit from 2500.00 to 2400.00. His credit limit remains 2500.00.

- Tom then makes a 50.00 purchase at Target using his debit card. Galileo checks the unheld balance available in the secured collateral account and confirms there are sufficient funds.

- Galileo approves the authorization and 50.00 is automatically pulled from the collateral account to cover the purchase.

- Tom’s credit limit is adjusted from 2500.00 to 2450.00, with 100.00 held for the credit purchase.

Your responsibilities

When you offer a Galileo Secured Credit product, your primary source of revenue for the product is the credit interchange that you receive from the card networks. Setting up and administering a secured credit product is a complex process, which may require a significant investment from you. Galileo can handle some tasks for you, such as account setup, processing, and Metro 2 file creation.

Learn more about the requirements for setting up a secured credit program in the Setup for Galileo Secured Credit guide.

Updated 6 months ago